Funding retirement is a top priority for most Canadians, and the Registered Retirement Savings Plan (RRSP) serves as the primary retirement savings vehicle for those who are not members of a workplace pension plan. Retirement savings should ideally be considered year-round, but the topic tends to attract the most attention in the first 60 days of each year as RRSP contributions made in that timeframe can be deducted on the previous year’s Income Tax and Benefit Return (T1).

How Much Can You Contribute to Your RRSP?

Canadians who are not enrolled in a workplace pension can generally contribute to their RRSP based on the following calculation:

A. Unused RRSP deduction room carried forward from the previous year.

Plus

B. The lesser of:

- 18% of earned income from the previous year; and

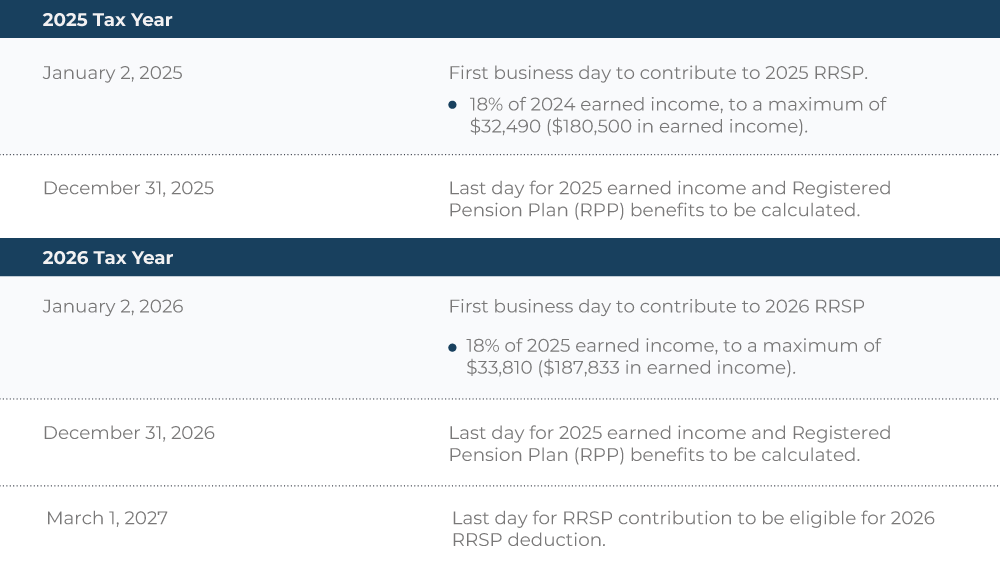

- The annual maximum limit, which is $33,810 for 2026 ($32,490 for 2025).

Less

C. Unused RRSP contributions carried forward from the previous year.

Plus

D. $2,000.

Understanding RRSP Contributions versus Deductions

RRSP contributions are funds deposited into your RRSP account using pre-tax dollars. However, an RRSP deduction refers to contributions that are reported on your T1, which reduces your taxable income for tax purposes. Not all RRSP contributions must be deducted in the year they are made; you can choose to defer to a future year.

Understanding the RRSP Deduction Limit and Available Contribution Statement

After filing your T1 tax return, the Canada Revenue Agency (CRA) sends a Notice of Assessment (NOA). For Canadians under age 71, the NOA includes the RRSP Deduction Limit and Available Contribution Statement (RRSP Statement). The RRSP Statement, which Canadians can also access through CRA’s My Account, is the best resource to verify available RRSP contribution room.

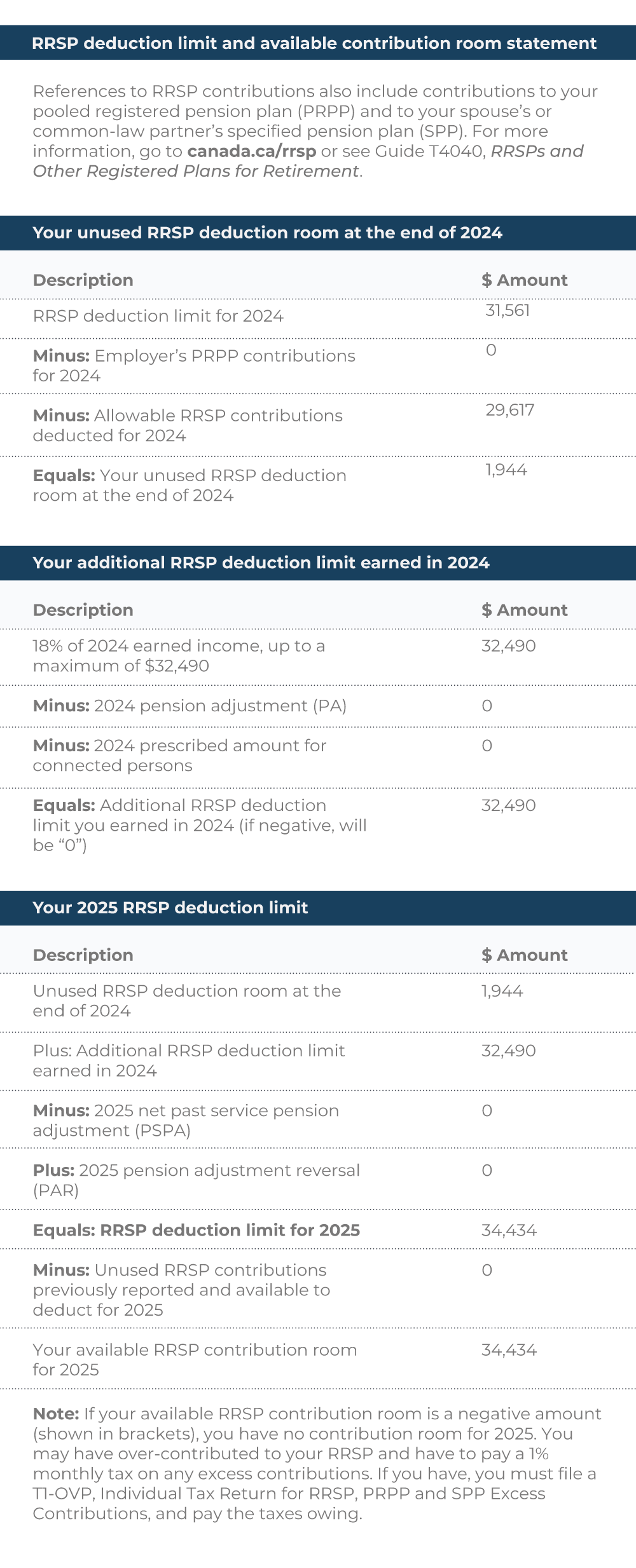

The format and terminology of the RRSP Statement have changed over recent years. To help understand the RRSP Statement, let’s step through Ms. Julie Rose’s RRSP Statement from her 2024 NOA.

The first section, “Your unused RRSP deduction room at the end of 2024”, outlines Julie’s 2024 RRSP deduction limit of $31,561 less her 2024 RRSP contributions deducted of $29,617. Accordingly, Julie has unused RRSP deduction room of $1,944 from 2024.

The second section, “Your additional RRSP deduction limit earned in 2024”, outlines Julie’s additional RRSP deduction room generated due to her earned income reported in 2024, less any contributions to a registered pension plan that would have been reported as a pension adjustment on her 2024 T4.

In 2024, Julie reported earned income of $200,000, so her additional RRSP deduction limit generated was $32,490, which was the lesser of:

$36,000 - 18% of earned income reported in 2024; and

$32,490 - the annual maximum limit.

The third section, “Your 2025 RRSP deduction limit”, summarizes Julie’s RRSP deduction limit from the first two sections and adjusts for any 2025 registered pension plan adjustments reflected on her 2024 T4, namely any net past service adjustment or pension adjustment reversal that may result from being a member of a registered pension plan. Lastly, any unused RRSP contributions she has not previously deducted is reflected.

Julie’s 2025 RRSP deduction limit of $34,434, was calculated by $1,944 from the first section plus $32,490 from the second section. As she did not have any unused RRSP contributions from prior years, and was not enrolled in a workplace registered pension plan, her available 2025 RRSP contribution room is $34,434 plus the allowable cumulative $2,000 overcontribution.

What if Julie’s NOA reflected $20,000 in unused RRSP contributions previously reported and available to deduct for 2025, what would be the impact to her available RRSP contribution room for 2025?

Her available 2025 RRSP contribution room would now be $14,434 ($1,944 + $32,490 - $20,000) plus the allowable cumulative $2,000 overcontribution allowance. This means Julie can make an additional $16,434 in RRSP contributions during the remainder of 2025.

Timing and Application of RRSP Contributions

The timing of RRSP contributions is important. RRSP contributions made in the first 60 days of a year can be reported as an RRSP deduction in either the previous, current or a future tax year. For instance, if Julie made RRSP contributions of $15,000 in November 2025 and $25,000 in January 2026, it appears at first glance that Julie has overcontributed to her RRSP. Fortunately, this is not the case. Her January RRSP contribution can be applied to her 2025, 2026 or future year, depending on her tax planning needs.

Additional RRSP Planning Considerations:

- Do you anticipate reporting a higher taxable income in the next few years?

If you expect to be in a higher tax bracket in the future, consider contributing to your RRSP now if you have the contribution room, thus shielding investment returns from tax, but deferring the deduction until a future year when it will result in greater tax savings. For example, a $15,000 deduction at a 30% tax rate generates $4,500 in tax savings, but at 43.5%, it saves $6,525.

- Do you anticipate the need to withdraw a contemplated RRSP contribution in the next 5 years?

If you anticipate the need to withdraw funds within five years, consider contributing to a TFSA instead. TFSA withdrawals are added back to your contribution room in the following year, but RRSP withdrawals are not, the RRSP contribution room is permanently lost. As well, TFSA transactions are after-tax, while RRSP contributions generate a tax deduction and withdrawals are taxable income.

- Do you, or your spouse, anticipate going back to school on a full-time basis?

If you or your spouse plan to enroll in a qualifying educational program at a qualified institution, the Lifelong Learning Plan (LLP) allows up to $10,000 per year and $20,000 in total to be withdrawn as a loan from your RRSP. The loan must be repaid over 10 years at a minimum of 10% annually. Ensure your RRSP has a balance of at least $20,000 for the maximum withdrawal.

- Do you anticipate buying or building a qualifying home as a first-time home buyer or a specified disabled person?

The Home Buyers’ Plan (HBP) is designed to assist those buying or home who are first-time owners or specified disabled persons. It allows up to $60,000 to be withdrawn as a loan from your RRSP. The loan must be repaid over 15 years starting in the second year after withdrawal. The RRSP must have at least $60,000 for the maximum withdrawal. Combined with the First Home Savings Account, individuals can save $100,000, and couples $200,000, towards their first home.

- Does it still make sense to consider a Spousal RRSP given eligible pension splitting with RRIFs after 65?

Yes, Spousal RRSPs are still valuable for tax planning, even with pension splitting of Registered Retirement Income Funds (RRIFs) allowed after age 65. They provide additional flexibility for splitting income and managing tax liabilities in retirement, especially if one spouse has significantly higher income or assets.

2025 and 2026 RRSP Key Dates and Facts

Connect with WealthLife Capital.

Please reach out to your Wealth Advisor to discuss your 2025 and 2026 RRSP contributions, and to address additional RRSP planning considerations you may have. We are here to support your retirement dreams becoming a reality.

Disclaimer

WealthLife Capital is an owner and partner in the Q Wealth Partnership. Portfolio Management services are provided by Q Wealth. Financial planning services are provided by WealthLife Capital. This document has been provided for information purposes only and is not intended to be relied upon as investment, financial, tax or legal advice. Please consult an independent legal or tax professional if considering the implementation of a planning strategy. The planning strategies and technical content are provided for the general guidance and benefit of our clients at the time of writing; however, we cannot guarantee the accuracy or completeness of the information contained herein.